Peapack Gladstone Bank

%20(2).png)

.png)

Applying for a mortgage is one click away!

Our newly enhanced mortgage application platform is easy to use and will walk you through the process every step of the way.

Get started today.

Digital Banking Tools and Financial Resources Designed to Help You

Review our library of insightful videos and educational tutorials to learn more about the suite of products and services that we provide to our clients.

%20_resized%20for%20ad%20tile.jpg)

The PGB Personal Banking Experience

Your PGB Personal banking experience is easier than ever with our newly designed, Online Banking portal and Mobile Banking app.

The intuitive design allows for easier online and mobile banking – find account balances and recent transactions, make transfers, deposit checks, pay bills, and more!

Your mobile provider may assess data and other usage charges, please check with your mobile provider.

Trust us a Big Deal: Commercial Banking Solutions

Watch our video to learn how we can help you achieve your financial goals.

Where you put your money matters.

Set and achieve your financial goals with a dedicated team and comprehensive financial advice. Our wealth management solutions are for high- and ultra-high-net-worth individuals, families, privately-held businesses, family offices, and not-for-profit organizations.

It takes passionate people of all

backgrounds to create a bank

that adapts to the needs of

our community.

The Peapack-Gladstone Financial Corporation Annual Report Website is LIVE!

For over a century, we've offered client-centric, single-point-of-contact private banking, which includes thoughtful insight along with customized and innovative wealth, commercial, personal and investment banking solutions. Discover how our team of experienced relationship managers are equipped to provide elevated, bespoke, and memorable experiences.

Hear what our clients have to say and see how our employees are investing in the communities where we live, work and play.

Making sure your deposits are protected.

The PGB Insured Liquidity Sweep program is an ideal cash sweep option for anyone seeking safety, security and liquidity.

Choosing the right credit card is easier than ever.

Enjoy important features like:

- Smart Chip Technology

- Mobile Purchasing Capability

- Plus much more!

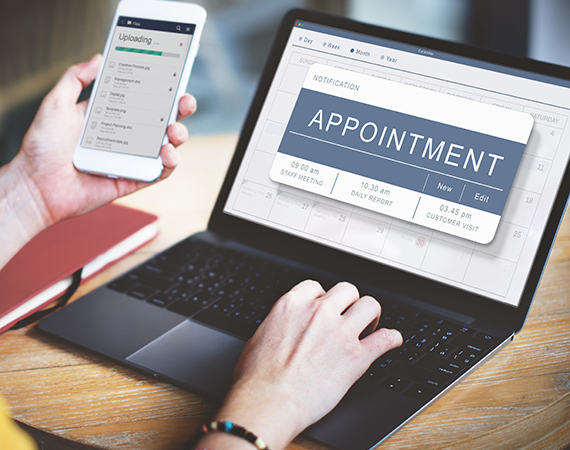

Did you know that you can schedule an appointment with us from the comfort of your home?

Scheduling an appointment is simple and easy. Click the button below to learn how.

Customized solutions for your Commercial and Industrial needs.

From acquisition, equipment, working capital and owner-occupied real estate financing, we provide solutions designed specifically to fit your needs, not ours.

Peapack Private was recently named one of Crain’s New York Business 2024 Best Places to Work in NYC. Congratulations to our entire NYC team for this well-deserved recognition.